Employees

Employees – Frequently Asked Questions

Information for employees who are new to the plan, getting ready to retire, or somewhere in between.

General Employee Information

Qualifying Service is employment (or combined periods of employment) that is unbroken by resignation, termination or retirement except for a temporary absence/layoff. A temporary absence/layoff is considered to be a period of employment if the absence/layoff does not exceed 54 consecutive weeks.

You have met the Rule of 80 when the combination of your age (minimum age 55) and qualifying service equals 80 or more (e.g., age 55 with 25 years of qualifying service or more). There is no early retirement reduction if you retire between the ages of 55 and 60 with the Rule of 80.

The CSSB is required by The Pension Benefits Act to have the Annual Employee Pension Statement available for the prior year by the end of June.

Members who are signed up for the CSSB Online Services will receive an email notification when their statement is ready and available for download.

If you are a new member and did not contribute to the pension plan in the previous year, you will not be able to run termination or pension estimates until our office receives the year end information from your employer.

If you find a discrepancy in your pensionable earnings, please contact your employer.

You can update your spouse/partner’s information (date of birth and name) and address by going to “Edit My Profile” in your Online Services account.

- You may have been on a leave of absence without pay. If you are on a leave of absence without pay, you do not contribute to the pension plan and your employer would not report pensionable service during this time.

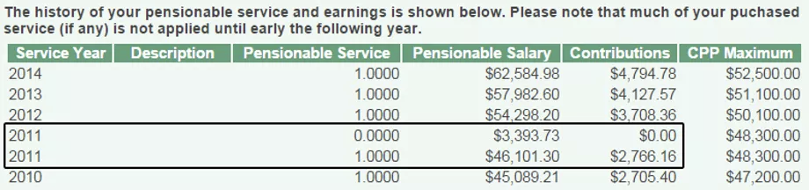

- You may have received retroactive pay which has been allocated back to the applicable year(s).

In the above case, this member received retroactive pay in 2011 which pertains back to a previous year. In the account history, these earnings are identified on a separate line.

No. Voluntary contributions are not permitted.

No. Borrowing contributions from a Registered Pension Plan is prohibited under the Income Tax Act and The Pension Benefits Act.

No. The Government of Canada’s Home Buyers’ Plan (HBP) applies only to withdrawals from Registered Retirement Savings Plans.

The Civil Service Superannuation Fund isn’t eligible under the HBP, and there are no provisions in the pension plan that permit funds to be withdrawn while still employed.

The exception to this would be for members who have non-locked-in funds in the Money Purchase Plan. Non-locked-in funds in the Money Purchase Plan may be removed at any time. Although the Money Purchase Plan isn’t an eligible plan under the HBP, a member could transfer their non-locked-in funds to an RRSP.